The Fuse

Equity futures are getting slammed this morning following big down moves from IBM, Meta and a few other names. Earnings have been pretty decent this quarter but perhaps after a 10% gain for the SPX 500 in Q1 maybe the good news was already priced in.

Interest Rates are bumping a bit higher as the next Fed meeting looms large. They are likely to keep rates steady next Wednesday but it’ll be more interesting to hear from Chair Powell after a few hot inflation reports this year.

Gold is rising slightly this morning as the metal continues its pullback from an overbought condition. Crude is slightly higher as well, silver above $24 per ounce. Today we’ll have a first look at Q1 GDP, jobless claims while tomorrow the important PCE report. We’ll be watching for higher inflation in both reports.

Earnings were very poor from Meta and IBM last night, or the reaction to them was poor. Chipotle put up a strong number as did Ford, but Meta’s talk about more spending is putting all the pressure on the markets. Later today more big reports from Microsoft, Alphabet, Snap, Intel, Roku and Dexcom.

Stocks were all over the place on Wednesday, plenty of volatility as the markets rose up strong to start the trading session, faded hard then rallied, faded again and finished mixed. However, earnings after the close from Meta and others are going to put heavy pressure in the indices today. We could have more volatility later in the week as more big earnings are due out and may drive investors crazy.

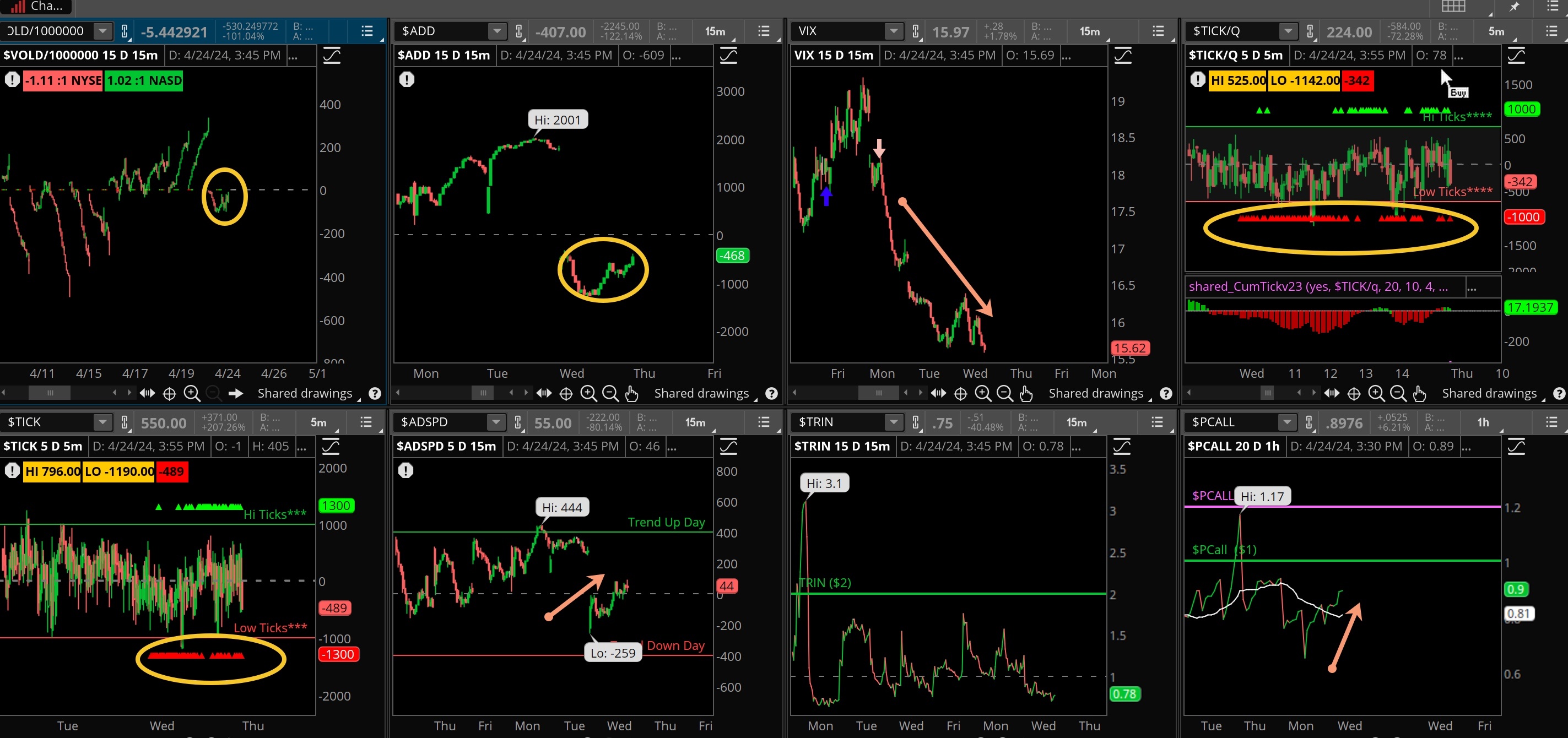

After two days of strong breadth the bears took control of this indicator. Thanks to the IWM being lower the decliners outdid the advancers. That is not a surprise, though we did see a buy signal arrive on Tuesday, that is now in question. Oscillators turned up Tuesday but have retreated and are near the flat line. Breadth shows the market is no longer oversold.

Volume was mixed, the DIA actually printed a distribution day while the Nasdaq was close, but make no mistake the big volume was to the downside all session long. If we see more distribution this week then those recent lows are in jeopardy for being clipped. Recent action has caused some publications like IBD to go ‘market in correction’. For good reason!

We had a swift move this week below 5K and then a resurgence above there, but that barely took the SPX to the 5,100 level before failing. The worry of course is the damage caused by Meta and if any buyers are willing to take some risk. It’s highly probably those lows around 4967 will be tested sooner or later.

The Internals

What’s it mean?

Something very different with the internals here from the prior days action. Notice much lower levels on VOLD and ADD, even though the market was relatively mixed end of day. A red flag! Ticks were lighting it up red one more time, especially on the Nasdaq early. That seemed to signal trouble ahead, and that is likely to be the case today. Put/calls remain on sell signals, too. It is difficult to play the earnings game especially in this environment.

The Dynamite

Economic Data:

Thursday:jobless claims, GDP advanced look Q1, pending home sales

Friday:PCE for March, Michigan sentiment

Earnings this week:

Thursday:RCL, NEM, MO,, CAT, LUV, AZN, MSFT, GOOGL, INTC, SNAP, OKU, WDC, DXCM, GILD, AEM

Friday:XOM, CVX, ABBV, HCA, CL, CHTR, BALL

Fed Watch:We have reached the point of ‘blackout’ period for the Fed speakers as they have become unified with their hawkish stance. Nothing on the schedule for this week. It seems almost unanimous the committee is less likely to cut rates in 2024, last week Chair Powell stated in no uncertain terms that inflation was not moving down as quickly as they wanted.

Stocks to Watch

Tesla – This stock has been a miserable performer this year and has been falling hard. Earnings are due out Tuesday after the close so we’ll be watching this carefully to see if traders respond with bearish behavior.

Semiconductor Stocks – This group was just hammered the past week, down some 10%. After some decent earnings from TSM and others it appears this has been a ‘sell the news’. NVIDIA’s poor performance contributed as did SMCI, but others’ charts are in a precarious position. Watching closely with Intel reporting Thursday.

Defense – Most names report this week and have started to improve. No doubt this was caused by the potential orders coming from the government, now spending has been approved and perhaps these companies will receive some contract benefits.

{kind=link}

{kind=link}