The Fuse

Happy Earth Day! US equity futures are higher this morning following a huge setback last week. As we enter the heart of earnings season with nearly 20% of the SPX 500 reporting this week alone, we’ll find out if buyers are truly seeing bargains after the recent 5% pullback from the recent highs. The Russell 2K has corrected more than 10% however as this leading index is in far worse shape.

Interest Rates are up a bit this morning as the 2 year bond tagged 5%, which is slightly below the fed funds mark. These bond holders have been selling the 2 year as well as longer duration bonds for the past few months, signaling more alignment with Fed speak about monetary policy. The futures market now sees aboug 1-1.5 rate cuts coming in 2024, and that is still in question. A couple of Fed speakers last week introduced the idea that 2025 would be the first rate cut. If anything, the next three meetings are off the table unless a trend in lower inflation arises.

Bulls were relieved there was no news over the weekend to put a dent into the markets. Friday’s action was a bit curious as it seemed stocks were washed out enough but some groups still struggled to move ahead. Gold is down sharply this morning, more than 2% while crude is also lower. Bitcoin was halved over the weekend, some of the crypto stocks are up nicely in the pre-market. Tesla cut prices on their models, the stock is down again today. They will report earnings Tuesday after the close.

Earnings this morning from Verizon and Zions bank, later today we’ll hear from Nucor, Cliffs, SAP, Cadence and a few other names. Tuesday AM is a big day for earnings that include UPS, GM, GE, PEP, LMT, SPOT, RTX and JBLU.

Stocks fell hard again Friday with the Nasdaq feeling the worst of the pain. Technology stocks were especially weak with the semiconductor names like NVIDIA having the most difficulty finding buyers. Demand may be slowing down as these stocks are well-ahead of their pace for 2024. Higher interest rates for longer continue to be the them as most small caps are anathema to this condition.

Breadth turned out modestly better under the circumstances with some groups like financials actually scoring a strong day. New lows continue to expand over new lows, the internals show some improvement but it is not lights out bullish. Oscillators are negative but not extreme here, still from the last extreme low a whopper of a rally can come at anytime.

Volume prints Friday were pretty heavy considering it was an option expiration day and with the heavy skew to the downside anyone who did not want stock put to them early (or who actually did) just sold shares or bought back their short options. The higher turnover on a down day notched one more distribution day for the indices, my good friends at Investor’s Business Daily have put the market in correction mode.

So much for 5K holding, we mentioned Thursday that would not be a big issue. 4,980 was the level to watch as that was the spot of a big gap to fill. That happened of course and the 4,900 level is waiting below. We could see a bit more extreme move to 4,850, just 2% lower from current levels. While many are poiting to this being a modest correction, we would agree to that for now but wary of a more scary downside happening soon.

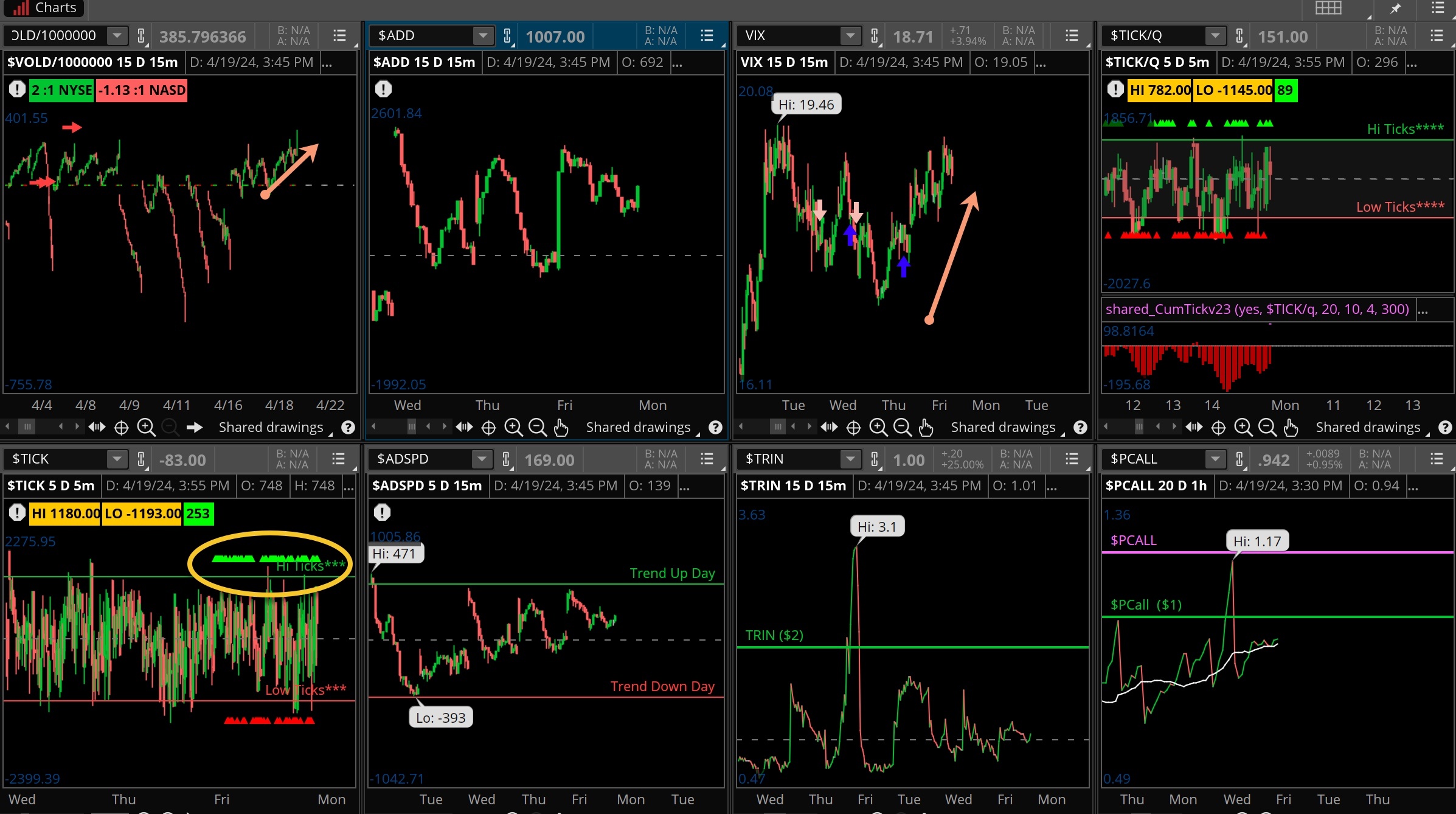

The Internals

What’s it mean?

The internals were not horrible, at least not matching up with the awful market move. Put/call remains elevated as does the VIX, but there was improvement in the VOLD and ADD. A start to better day, potentially. Ticks remain mixed but at least on the NYSE the green dominated the sellers. If this was just a short respite then the sellers might be back for more this week. Watching rates carefully this week.

The Dynamite

Economic Data:

Monday:n/a

Tuesday:SPX global PMI, new home sales

Wednesday:oil inventories, durable goods orders

Thursday:jobless claims, GDP advanced look Q1, pending home sales

Friday:PCE for March, Michigan sentiment

Earnings this week:

Monday:VZ, ZION,, NUE, CLF, SAP, CDN

Tuesday:GM, UPS, GE, PEP, LMT, SPOT, RTX, JBLU, TSLA, V, ENPH, TXN, BHI, STX

Wednesday:BA, T, HUM, GD, BSX, BIIB, META, IBM, F, CMG, NOW, VKTX, LRCX, CLS, ALGN

Thursday:RCL, NEM, MO,, CAT, LUV, AZN, MSFT, GOOGL, INTC, SNAP, OKU, WDC, DXCM, GILD, AEM

Friday:XOM, CVX, ABBV, HCA, CL, CHTR, BALL

Fed Watch:We have reached the point of ‘blackout’ period for the Fed speakers as they have become unified with their hawkish stance. Nothing on the schedule for this week. It seems almost unanimous the committee is less likely to cut rates in 2024, last week Chair Powell stated in no uncertain terms that inflation was not moving down as quickly as they wanted.

Stocks to Watch

Tesla – This stock has been a miserable performer this year and has been falling hard. Earnings are due out Tuesday after the close so we’ll be watching this carefully to see if traders respond with bearish behavior.

Semiconductor Stocks – This group was just hammered the past week, down some 10%. After some decent earnings from TSM and others it appears this has been a ‘sell the news’. NVIDIA’s poor performance contributed as did SMCI, but others’ charts are in a precarious position. Watching closely with Intel reporting Thursday.

Defense – Most names report this week and have started to improve. No doubt this was caused by the potential orders coming from the government, now spending has been approved and perhaps these companies will receive some contract benefits.

{kind=link}